Floatplane & Seaplane Financing · Amphibious · Flying Boats · Float Conversions

Floatplanes and seaplanes are among the most rewarding aircraft to own — and among the most diverse, with various float configurations, hull construction, and even amphibious certifications. FLYING Finance works with lenders who know the difference between a Super Cub's Edo 2000 and versatile Wipline 3450's.

Closed & Funded — Certified Piston

How the financing works

A Cessna 185 on straight floats and a Cessna 185 on wheels are the same airframe with very different collateral profiles. The float installation — manufacturer, model, amphibious vs. straight, age, and documentation — affects market value, buyer pool depth, and lender appetite. Here is what you need to know before you apply.

Every float installation requires an STC (Supplemental Type Certificate) that must travel with the aircraft. The STC authorizes the specific float model on the specific airframe. Lenders will verify that the STC is current, matches the installed floats, and that the float weight and balance documentation has been updated. Missing or mismatched STC paperwork is the most common floatplane financing complication — verify before you make an offer.

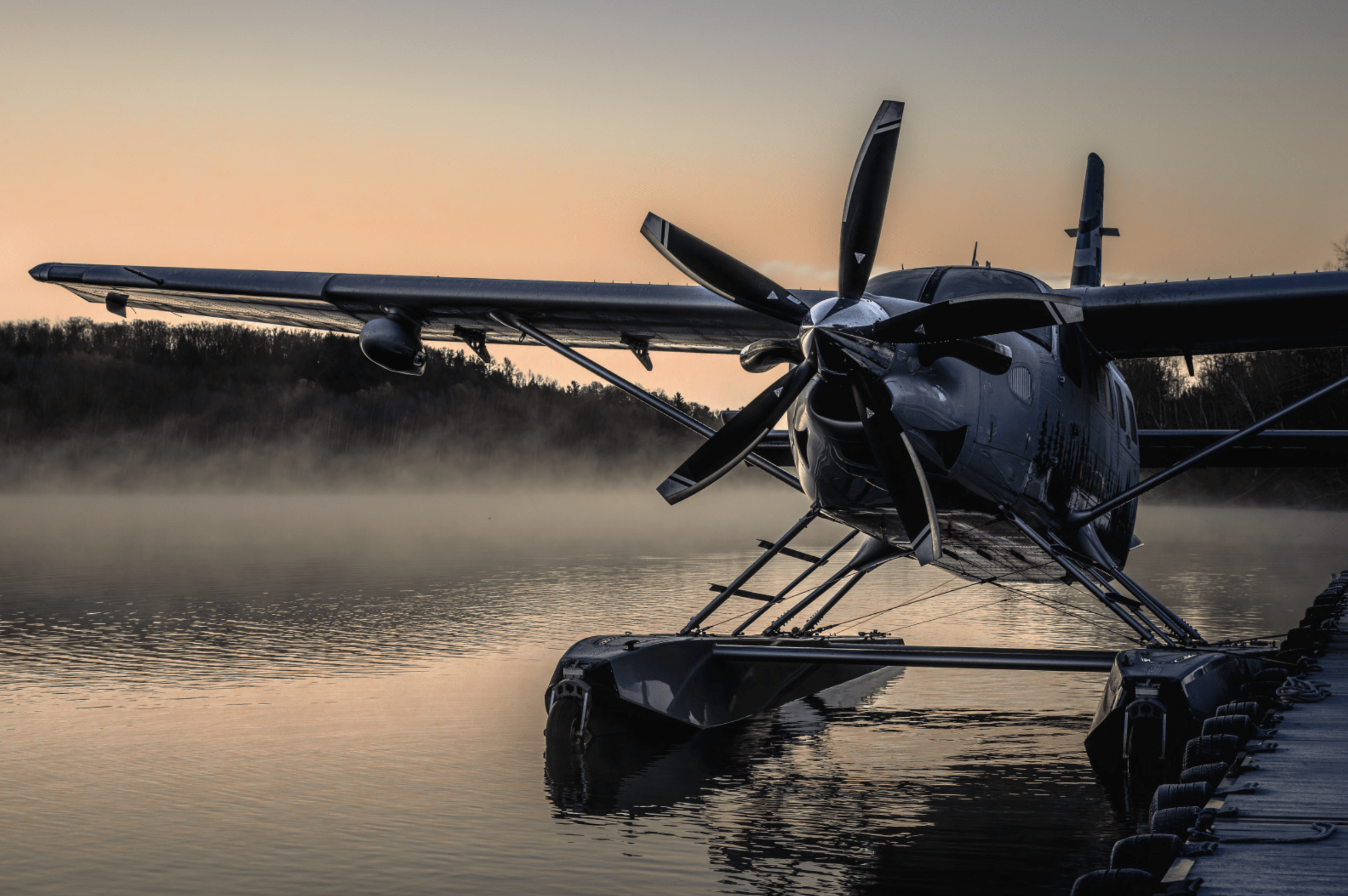

Amphibious floats (retractable wheels built into the floats) typically add $40,000–$100,000+ to an aircraft’s value and significantly broaden the buyer pool — the aircraft can operate from both land and water. Straight floats narrow the buyer pool to water-access operators only. Lenders generally prefer amphibious configurations for exactly this reason. Either is financeable; the amphibious aircraft typically qualifies for better terms.

Water operation accelerates corrosion on airframes, engines, and control surfaces. Lenders who specialize in floatplanes will ask for corrosion inspection records — specifically whether the aircraft has been treated with corrosion inhibitor, when the last corrosion inspection occurred, and the condition of float attachment points. An aircraft with a documented corrosion prevention program and annual inspections closes faster and on better terms than one without records.

Not all aviation lenders have appetite for floatplanes. Some treat float-equipped aircraft as a non-standard collateral category and either decline or apply significant rate adders. FLYING Finance works specifically with lenders who are active in the floatplane market and understand the valuation nuances. Submitting a floatplane application to a lender without floatplane experience wastes time and generates unnecessary credit inquiries. Let us match you to the right lender before you apply.

Aircraft commonly financed

The most common floatplane in Alaska and the Pacific Northwest. Deep pre-owned market, strong lender familiarity. Standard certified piston terms on documented examples with current STC.

Legendary bush aircraft with a cult following and a strong resale market. PT6 turbine conversions (Vazar, Viking) significantly affect value and financing terms. Contact us before pursuing a turbine Beaver — the loan structure differs from the piston version.

Six-seat capacity on floats with a cargo door. Popular for charter, lodge support, and remote access. Strong resale. Standard certified piston terms. Amphibious configuration strongly preferred by lenders.

The quintessential backcountry floatplane. Part 23 certified, standard piston terms. Older production dates (1949–1994) trigger age formula on some lenders — contact us before pursuing a specific airframe to confirm terms.

Factory float options available from Maule. One of the few certified four-seat aircraft with genuine STOL performance on floats. Standard certified piston terms. See the backcountry financing page for the full Maule profile.

LSA flying boats finance on LSA terms — 15-year max amortization, 20% down. The Icon A5 has a niche but active market. MOSAIC provisions effective July 2026 expand the eligible pilot pool. Contact us for current lender appetite on specific models.

Float configuration adds complexity but not necessarily cost. Well-documented floatplanes with current STCs and corrosion records finance on the same terms as their land-based counterparts.

Common questions

Yes, with the right lender and proper documentation. Certified floatplanes finance on standard certified piston terms — same rates, same amortization — provided the float installation has a current STC, corrosion documentation is in order, and the aircraft has a current annual. The critical variable is lender selection. Submit a floatplane application to a lender without floatplane experience and you may face unnecessary scrutiny or an outright decline. FLYING Finance routes floatplane applications specifically to lenders active in this market.

They can. Straight floats narrow the buyer pool to water-access operators, which some lenders view as reduced liquidity. Most lenders will still finance straight-float aircraft but may require a larger down payment — typically 20% vs 15% for amphibious. Amphibious configurations are preferred because the aircraft can operate from both land and water runways, which broadens the resale market. If you are choosing between an amphibious and straight-float aircraft, the amphibious will typically qualify for better financing terms.

Standard aircraft documentation plus float-specific requirements: current STC for the float installation on the specific airframe serial number; float weight and balance documentation; current annual inspection covering float attachment points; corrosion inspection records; airframe, engine, and propeller logbooks; FAA registration; hull insurance binder (marine coverage required); and signed purchase agreement. Hull insurance on floatplanes typically requires a seaplane endorsement — arrange this before you apply.

The Beaver is one of the most recognized bush aircraft in the world and has a deep, active market. Piston Beavers (R-985 Wasp Junior) finance on standard certified piston terms with a strong lender community. Turbine conversions — Vazar, Viking, Soloy — change the collateral profile significantly: turbine terms may apply, and the conversion STC and logbooks must be complete. Contact us before pursuing a turbine Beaver — the financing picture is quite different from the stock piston aircraft and depends heavily on which conversion is installed.

Yes. Floatplane hull insurance requires a seaplane rating endorsement or equivalent — your standard private pilot hull policy will not cover water operations without it. Most lenders require proof of insurance before closing, so arrange your seaplane insurance early in the process. Premiums for floatplanes are generally higher than land aircraft of equivalent value due to the operating environment. Budget for this before you finalize your purchase price and loan structure.

Yes — this is typically structured as a refinance of the existing aircraft plus the float conversion cost, or as a separate avionics/equipment loan depending on the lender. The float installation must have a valid STC, and the total loan-to-value after conversion must meet lender requirements. Contact us before you order the floats — we can structure the financing ahead of the installation so funds are available when the conversion is complete.

Tools & resources

Model a specific floatplane transaction or get pre-approved before you commit to a pre-buy.

Amelia · FLYING Finance AI specialist

"Floatplane financing is one of the more nuanced categories in general aviation — lender selection and documentation are everything. Ask me about float STC requirements, how amphibious vs. straight floats affect your terms, what a Beaver or C-185 loan looks like, or how to structure a float conversion."