✓

This aircraft has closed. We're sharing it because EAB financing is widely misunderstood — and more buyers qualify than realize it.

Build Category

EAB

Experimental Amateur-Built

Engine

Lycoming IO-540

260 hp, typical config

Rate at Closing

6.59%

Certified rate

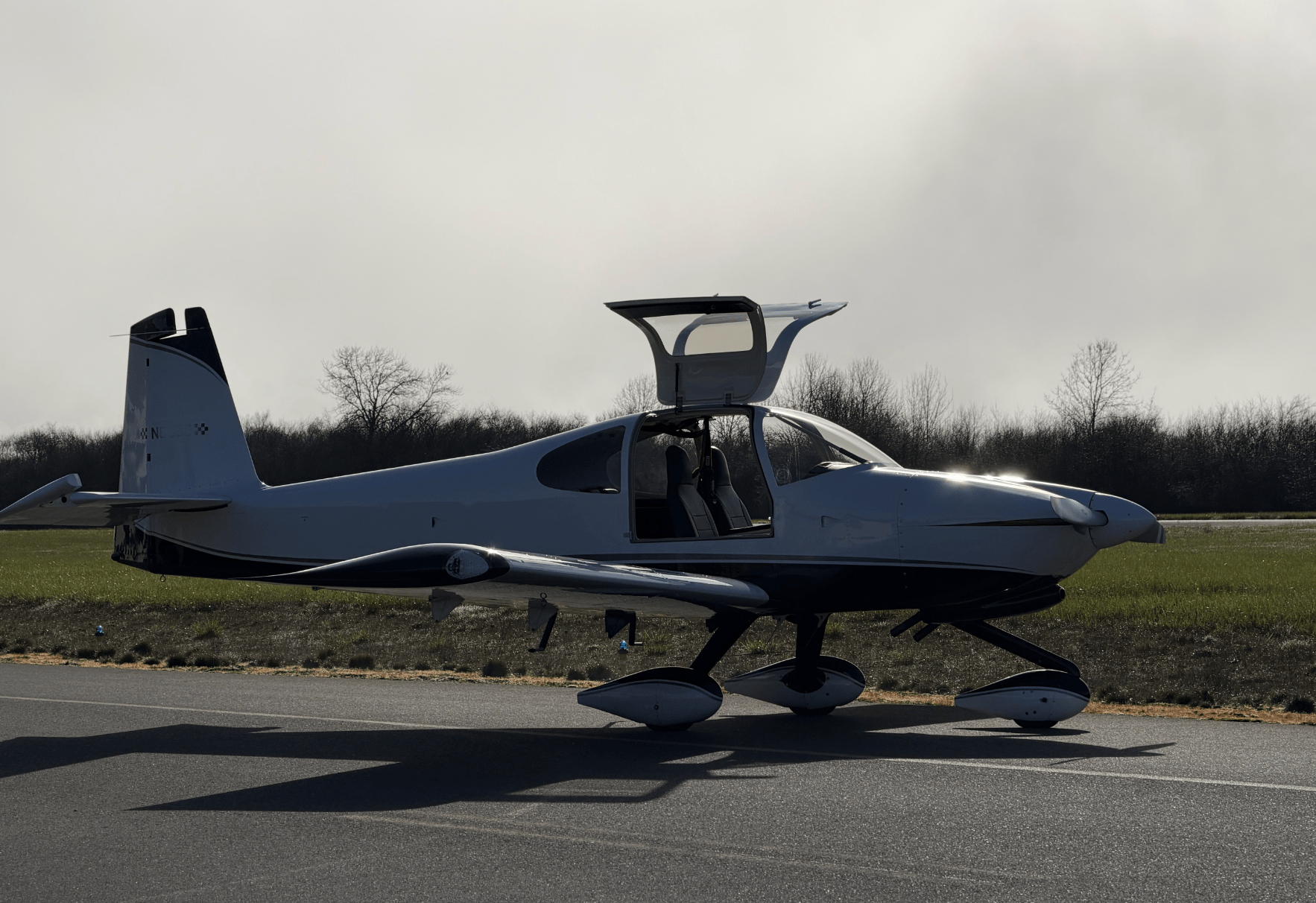

About the Van's RV-10

The Van's RV-10 is a four-seat, all-metal kit aircraft — the largest in the RV series — designed around a Lycoming IO-540 engine in the 260 hp configuration. Unlike the smaller two-seat RV models, the RV-10 carries four adults in side-by-side seating and is built for cross-country use, with cruise speeds typically in the 160–175 knot range depending on engine configuration and altitude.

Build quality and documentation vary significantly across individual RV-10 aircraft, which is one reason lender requirements for EAB aircraft involve closer scrutiny than certified types. A completed, well-documented 2008 RV-10 with a known engine history and modern G3X avionics lists for upwards of $325,000 to $350,000.

How We Financed This Aircraft

This transaction closed at 6.59% — a certified rate, not an EAB-specific premium. The reason this worked is lender matching. FLYING Finance paired this borrower with a lender who specifically knows Van's aircraft and has deep familiarity with the RV-10 in particular. That lender familiarity — confidence in valuations, build quality norms, and resale patterns for this specific model — is what drove certified rate treatment.

Not every EAB transaction qualifies for certified pricing. The EAB lender pool is smaller than for certified types, and knowing which lenders accept which experimental aircraft — and at what terms — is where an experienced broker adds direct value. See our EAB financing page and our live rates page for current figures.

EAB financing is available — and when you're matched with a lender who knows the model, it can close at rates comparable to certified aircraft.

What to Expect in the Process

For an RV-10 or similar EAB transaction, the process typically looks like this:

- Pre-qualification: Same financial requirements as certified piston — credit, income, and down payment. EAB does not require a stronger financial profile, just more scrutiny on the aircraft side.

- Aircraft documentation: Builder log, operating airworthiness certificate, current condition inspection, and maintenance records. These are the baseline requirement for any EAB transaction — the same standard required alongside acceptable credit, LTV, and a satisfactory pre-purchase inspection.

- Lender matching: This is where EAB diverges from certified. FLYING Finance identifies lenders with specific experience in the aircraft type, which directly affects available terms.

- Appraisal: An appraiser experienced with experimental aircraft assesses the aircraft individually. Build quality, avionics, and engine time all affect value.

- Insurance: Available for EAB aircraft, but underwriters evaluate type-specific experience more closely than for certified singles.

- Closing: EAB transactions typically run 14–28 days due to the additional steps involved.

See our loan process page for a full step-by-step overview.

Questions Buyers Ask About EAB Financing

Can experimental aircraft actually be financed? +

Yes. FLYING Finance works with lenders who specifically accept Experimental Amateur-Built aircraft. Not all aviation lenders do — which is one reason working with a broker who knows the EAB lender pool matters. Well-documented Van's aircraft like the RV-10, RV-7, and RV-9 are among the most commonly financed EAB types.

Can an EAB aircraft close at a certified piston rate? +

Yes — this transaction did. The key is being matched with a lender who knows the specific model. A lender with deep familiarity with Van's aircraft and the RV-10 can price the risk more precisely, which is what enabled certified rate treatment here. Not every EAB deal qualifies, but it happens more often than buyers expect when the right lender match is made.

What documentation does a lender require for an EAB purchase? +

At minimum: operating EAB airworthiness certificate, builder log, complete ownership chain documentation, current condition inspection sign-off, and maintenance records. This is the baseline for any EAB transaction — the same standard required alongside acceptable credit, LTV, and a satisfactory pre-purchase inspection.

Does it matter if I'm not the original builder? +

No — you do not need to be the original builder to purchase and finance an EAB aircraft. The operating airworthiness certificate transfers with ownership. What matters is that the documentation chain is intact and the aircraft has a valid, current airworthiness certificate.

What is the minimum loan amount for an EAB aircraft? +

Most lenders set a minimum of $35,000–$50,000 for EAB transactions. For a well-equipped RV-10 in the $100,000–$150,000 range, financing is straightforward to structure when the right lender match exists.

How does EAB insurance work? +

EAB aircraft are insurable. Underwriters evaluate type-specific experience and transition training more carefully than they do for certified singles. Insurance for an RV-10 is available for pilots with appropriate total time and experience — premiums vary more than they do for certified aircraft.

Related Resources