President Trump’s Carefully Choreographed Interest Rate Strategy Collides with the Iran Conflict, Upending the 2026 Outlook for Everything from Mortgages to Turboprops

The playbook was elegant in its simplicity. Install a hawkish Federal Reserve Chair to maintain credibility, engineer a soft landing through managed inflation and a cooling labor market, then deliver politically timed rate cuts in the second half of 2026—just in time for the midterm elections. Republicans would campaign on falling mortgage rates and a revitalized economy. President Trump would cement his legacy on his own terms.

That playbook is now in flames, torched by the same military strikes on Iran that were supposed to demonstrate American strength.

As oil prices surge past levels not seen in years—with gasoline now averaging a dollar more per gallon than before the conflict began—the calculus that once seemed so precise has unraveled. The Federal Reserve, which had been carefully positioning for potential rate reductions, now finds itself trapped between the twin pressures of resurgent inflation and an economy that could tip into slowdown. Far from cutting rates, officials are signaling they may need to hold steady indefinitely—or worse.

“I understand why many Americans are frustrated with inflation,” Fed Vice Chair Philip Jefferson acknowledged in a recent speech in Dallas. “Following pandemic disruptions, inflation has remained above the Fed’s 2.00% target for five years.”

The understatement was notable. With the personal consumption expenditures price index running at 2.8% and core inflation stuck at 3.0%, the administration’s carefully managed narrative about conquering inflation has given way to renewed anxiety at kitchen tables across America.

Executive Summary: The 2026 Q2 Outlook

- The Narrative Shift: The anticipated 2026 “Soft Landing” and timed rate cuts have been replaced by a “Stagflation” hedge as oil clears $110/bbl.

- The Interest Rate “Stare-Down”: The Fed is currently trapped; resurgent energy-driven inflation (Core 3.0%) has effectively paused the rate-cut cycle for the foreseeable future.

- The Efficiency Premium: General Aviation is shifting from a “Speed” market to an “Efficiency” market. Assets with superior fuel-burn profiles (DA62, TBM 960, PC-12) are seeing increased residual value stability.

- The Counter-Cyclical Play: Market hesitation is creating a “Buyer’s Window.” As institutional fleet orders pause, high-fidelity delivery slots are opening for private buyers with ready capital.

The Dual Mandate Dilemma

The Federal Reserve’s challenge has rarely been starker. Its dual mandate—stable prices and maximum employment—now threatens to pull in opposite directions.

The March jobs report offered some relief: 178,000 jobs added, beating expectations, with unemployment ticking down to 4.3%. Under normal circumstances, such numbers would give policymakers room to maneuver. But these are not normal circumstances.

“As a monetary policymaker I confront an outlook where there is downside risk to the labor market and upside risk to inflation,” Vice Chair Jefferson said. “While that is a potentially challenging situation, I am confident that our current policy stance is well positioned to respond to a range of outcomes.”

That confidence may be tested. Governor Michael Barr, speaking at the Brookings Institution, was more direct about the risks: “We have had five years now of inflation at elevated levels, and near-term inflation expectations have risen again, so I am particularly concerned that yet another price shock could increase longer-term inflation expectations.”

The danger Barr described is the scenario that keeps Fed officials awake at night: that a series of supply shocks—tariffs, labor shortages, and now an energy crisis—could lead Americans to simply expect higher inflation as the new normal. Once that psychology takes hold, it becomes self-fulfilling.

Over the past eighteen months, the Federal Open Market Committee had lowered the target range for the policy rate by 175 basis points (1.75%). Those cuts were supposed to pave the way for more to come. Instead, bond markets and aircraft lenders are now pushing in the opposite direction. Treasury yields rose after the jobs report, with the 10-year Treasury climbing to 4.35%. Investors have steadily pushed out their estimates for when, or whether, further rate cuts will materialize.

For the average American considering a home purchase, a car loan, aircraft or business financing, the message is clear: the lower rates that seemed within reach are receding.

Energy Prices Cast a Long Shadow

The economic logic of oil shocks is brutally straightforward. Energy products directly represent about 7% of total consumer spending, but petroleum costs are embedded throughout the economy—in transportation, manufacturing, agriculture, and food production. When oil prices spike, the pain radiates outward.

The effects are already visible. In France, nearly 10% of petrol stations have experienced shortages. U.K. businesses surveyed by the Bank of England in March expect to raise prices at a faster rate than before the conflict began. Food industry groups warn that U.K. food inflation could reach 9 to 10 percent by year’s end, up from 3.2%.

Texas as a Hedge: The Domestic Energy Buffer

The United States is better positioned than Europe or Asia — it leads the world in crude oil and natural gas production and is a net energy exporter. Texas alone accounts for roughly 15% of the state’s economic output through energy production, transportation, and processing.

But no region is immune. The longer prices remain elevated, the more households will face difficult tradeoffs: less dining out, reduced retail spending, potentially higher debt loads.

“When gasoline prices jump, families—especially those with lower incomes who spend a larger share on essentials—have less money for everything else.” – Vice Chair Jefferson.

The agricultural sector faces particular strain. Fertilizer prices have soared since Iran’s closure of the Strait of Hormuz disrupted a critical transit point for a third of the world’s fertilizer supply. The cost of two widely used nitrogen fertilizers shot up by 20 and 50 percent in the first weeks of the war. For Iowa corn farmers preparing to plant, the timing couldn’t be worse. One farmer facing $13,000 in additional fertilizer costs over just two days captured the desperation: “What pot does that come out of? Fertilizer price, we can’t control. Fuel price, we can’t control. Where is it all going to end up? We don’t know.”

For energy-producing states, there may be offsetting benefits—more drilling activity, higher wages for energy workers, stronger profits for oil companies. But nationally, the calculus is less favorable. And politically, rising gas prices are poison for any administration.

A Political Paradox

The irony is not lost on either party. President Trump’s strike on Iran was intended to project American power and potentially resolve a longstanding geopolitical threat. The economic consequences, however, are handing Democrats their most potent argument in years.

After months of Republican messaging about fiscal discipline and economic stewardship, the opposition now has a simple rejoinder: gas is over $4 a gallon, inflation is rising, and the administration’s policies are directly responsible. The affordability argument that Democrats struggled to articulate amid strong job numbers and stock market gains now writes itself at every gas station in America.

John Williams, president of the Federal Reserve Bank of New York and a close ally of Fed Chair Jerome Powell, acknowledged the bind: the conflict “could result in a large supply shock with pronounced effects that simultaneously raises inflation, through a surge in intermediate costs and commodity prices, and dampens economic activity.”

This is the stagflation scenario that haunted the 1970s, when oil shocks sent the economy spiraling. Officials are quick to note that conditions today differ substantially – the U.S. produces far more energy domestically than it did a half-century ago. But the political dynamics remain unchanged: voters punish incumbents when their cost of living rises.

The administration’s response has been multifaceted. Trump lifted sanctions on fertilizer sales from Belarus and Venezuela to ease the price surge and promised more aid to farmers. The White House’s new budget request seeks approximately $1.5 trillion for defense in the 2027 fiscal year, a roughly 40% increase from current spending, coupled with $73 billion in cuts to domestic programs.

Yet the carefully sculpted 2026 outlook has fundamentally changed. Markets have wavered following Trump’s pledge to hit Iran “extremely hard,” sending the U.S. oil benchmark soaring. Asian equities have fallen as Trump signals further military strikes. The dollar has strengthened against most currencies, but investor sentiment swings wildly with each presidential statement.

General Aviation: From Tailwind to Headwind

Nowhere is the shift in economic sentiment more visible than in the general aviation market, where optimism that built throughout 2025 now confronts a far more uncertain horizon.

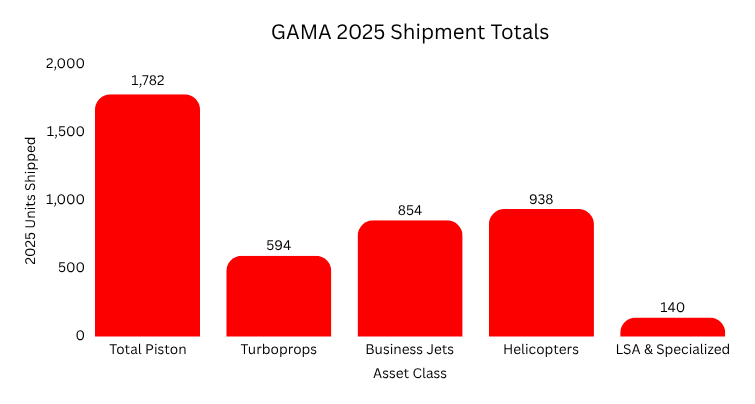

The numbers from the General Aviation Manufacturers Association tell a story of strength entering the new year. Total civil aviation shipments for 2025 reached 4,308 units worldwide, generating $35.7 billion in billings. Business jet deliveries totaled 854 units across manufacturers. The piston market, often a bellwether for broader economic confidence, showed sustained demand.

The domestic market wasn’t just holding—it was accelerating. Textron Aviation moved 639 units across its Cessna and Beechcraft lines, generating nearly $3.8 billion in revenue. Gulfstream’s 158 deliveries produced over $10 billion in billings alone. Embraer shipped 155 aircraft worth $2.5 billion. Bombardier delivered jets worth nearly $8 billion.

The helicopter market showed similar vitality. Worldwide rotorcraft shipments were led by Airbus Helicopters with 373 deliveries worth $2.6 billion and Bell with 169 units generating $850 million.

Coming into 2026, industry executives cited multiple reasons for optimism. Tariff volatility that had whipsawed supply chains throughout 2024 appeared to be stabilizing. Most importantly, interest rates had been trending lower, making aircraft financing more accessible for both individual buyers and charter operators.

Now those assumptions require revision.

The Financing Factor

While energy costs dominate the headlines, the April 15th liquidity squeeze is the invisible hand in the market. Sophisticated buyers are currently leveraging the 2026 bonus depreciation schedule as a tax-shield against volatile Q1 business earnings, making the ‘Net Cost’ of acquisition significantly lower than the ‘Sticker Price’ suggests.

Aircraft purchases, whether a training aircraft or a large cabin jet, are acutely sensitive to interest rate movements. Most buyers finance significant portions of their acquisitions, often up to 85%, meaning that even modest rate increases translate directly into higher monthly payments and reduced purchasing power.

The calculus is straightforward. When rates were declining, prospective buyers had incentive to act quickly before financing became cheaper, while also feeling confident that resale values would hold. With rates now uncertain or potentially rising, that psychology reverses. Buyers defer decisions. Flight schools, fractional operators and charter companies recalculate fleet expansion plans. Manufacturers face the prospect of softening order books.

Energy costs compound the challenge. Jet fuel prices track crude oil with predictable correlation. Higher operating costs squeeze margins for charter operators and corporate flight departments, reducing demand for new aircraft. Flight training operations face the same pressure, fuel prices affect the economics of everything from primary instruction to aerobatic training without regard to whether your engine takes Jet A, 100LL or Mogas.

The regional dynamics matter as well. While North America absorbs the largest share of deliveries, significant markets exist in Europe, Latin America, and Asia Pacific. European economies are being hit harder by energy disruptions than the United States, given their greater dependence on imported oil and gas, and taking this latest disruption on the heals of the Ukraine war implications. Regions more dependent on energy imports, as Vice Chair Jefferson noted, “may see economic activity and inflation more negatively affected than the U.S.” Weaker demand from foreign buyers would ripple back to American manufacturers.

What the Fed Is Watching

For aviation industry executives trying to plot strategy amid uncertainty, the Fed’s own guidance offers clues, though maybe not comfort.

Officials have emphasized that the current policy stance leaves them “well positioned to determine the extent and timing of additional adjustments” based on incoming data. Translation: they will not commit to a direction until the fog clears.

Vice Chair Jefferson acknowledged that the disinflationary process could resume “once higher tariffs are no longer pushing up consumer prices” and that strong productivity growth might help bring inflation down. But he immediately added the caveat: “The ongoing trade policy uncertainty and geopolitical tensions, however, pose upside risk to my inflation forecast.”

Governor Barr was more explicit about the waiting game: “Given the considerable uncertainty about the potential effects of developments in the Middle East on our economy, as well as the other factors I mentioned, it makes sense to take some time to assess conditions. Our current policy stance puts us in a good place to hold steady while we evaluate incoming data, the evolving forecast, and the balance of risks.”

For aircraft buyers contemplating major purchases, “wait and see” is a directive, not just a monetary policy stance.

Fed Chair Jerome Powell himself, at a recent event, acknowledged the dilemma: “You can have a series of these supply shocks and that can lead the public generally, businesses, price setters, households, to start expecting higher inflation over time. Why wouldn’t they?” Yet despite this risk, Powell did not convey immediate urgency, saying instead that the Fed’s policy was “in a good place for us to wait and see how that turns out.”

The Duration Question

Everything depends on how long the conflict lasts and how severely it disrupts global oil flows.

Fed officials have been clear on this point. A short period of disruption, Vice Chair Jefferson said, “is unlikely to have a noticeable effect on the economy beyond a quarter or two.” But a sustained energy price shock “could have material implications.”

New York Fed President Williams forecast that unemployment would tick down from current levels and inflation would end the year around 2.75%. That is roughly where it is now. That relatively sanguine projection assumes the conflict proves short-lived and global oil flows return to prior levels. We get back to normal.

If that assumption proves wrong, all bets are off.

The Strait of Hormuz remains largely closed to international shipping, with crossings reduced to a trickle since the conflict began. A French-owned container ship recently made the first known transit by a major European shipping group since early March, using a newly approved route through Iranian waters that Lloyd’s List has dubbed the “Tehran Toll Booth.” Most vessels crossing the strait have been linked to Iran or countries such as the UAE, India, China, or Saudi Arabia.

Resiliency in Disruption

The domestic general aviation industry, which has proven remarkably resilient through trade wars, pandemic disruptions, and monetary policy gyrations, now faces a test it did not anticipate. The momentum that carried it into 2026 remains real: order backlogs, operational demand, and underlying economic fundamentals have not disappeared. But the tailwinds have shifted.

For President Trump, the political calculus is equally stark. The meticulous choreography that was supposed to deliver rate cuts and economic good news ahead of November has been disrupted by decisions made in the Situation Room, not the Oval Office. His new Fed Chair’s hawkish instincts, which once seemed like prudent positioning, now look like an impediment to the rate relief that voters are expecting.

Republicans had planned to run on economic competence. Democrats are preparing to run on gas prices. The midterms are seven months away, and the outlook that seemed so carefully sculpted has become something else entirely: uncertain.

Finding Opportunity in Uncertainty

Yet for sophisticated aircraft buyers, periods of market uncertainty have historically created opportunity. The current environment, for all its challenges, is no exception.

Strategic Tooling: In a high-fuel-cost environment, the delta between “Planned Burn” and “Actual Burn” is the difference between a viable mission and a grounded asset. Use our Aircraft Comparison Engine to benchmark the real-world efficiency of your next acquisition against 2026 energy benchmarks.

The fundamentals that drove general aviation strength through 2025 have not evaporated. Total aircraft billings exceeded $35.7 billion worldwide last year. Manufacturers remain committed to production schedules. And critically, the demographic and operational factors driving demand—aging fleet replacement, the continued growth of fractional ownership, and corporate appetite for time-efficient travel—persist regardless of what happens in the Persian Gulf.

For buyers with strong balance sheets and patient capital, hesitation among competitors translates into negotiating leverage. When financing committees at fractional operators pause expansion plans, delivery slots that would otherwise be unavailable open up. When prospective buyers defer decisions awaiting rate clarity, manufacturers face pressure to accommodate those who are ready to move forward.

The order backlog dynamics across major manufacturers suggest where opportunities may emerge. Gulfstream’s deliveries of 158 aircraft in 2025 generated over $10 billion in billings, but demand for large-cabin jets consistently outstrips supply. Buyers who can commit during uncertain periods often secure preferential positions. Similarly, Bombardier’s 71 Challenger deliveries and substantial Global series shipments reflect a production cadence that continues regardless of macroeconomic headlines.

In the turboprop segment, the equation favors operators focused on operational economics. Turboprops consume less fuel than jets, making them relatively more attractive as energy costs rise. Pilatus, which delivered 132 aircraft including 82 PC-12s and 50 PC-24 jets worth $1.2 billion, has built its market position precisely on efficiency arguments that resonate in high-fuel-cost environments. Daher’s 76 deliveries, including 51 TBM 960s, demonstrate similar appeal.

The piston market tells a comparable story. Textron Aviation’s 191 Skyhawks and numerous other piston aircraft shipped to flight schools and private owners represent a training pipeline that doesn’t pause for geopolitical uncertainty.

There are even bright spots emerging from the energy crisis itself. Tesla sold slightly more cars in the first three months of 2026 than a year earlier – 358,023 vehicles globally compared to 336,681 during the same period last year, even without the tax credits that expired last Autumn – suggesting that higher fuel costs are prompting more consumers to consider electric vehicles. Hyundai’s electric Ioniq 5 sales rose 13% in March. The principle applies across transportation: when operating costs rise, efficiency becomes more valuable.

For potential buyers evaluating purchase options, a broader, more grounded sentiment should be employed. Energy prices will fluctuate. Interest rates will eventually find a new equilibrium. The question is whether the operational requirements that justify business aviation – time savings, schedule flexibility, access to underserved markets – have changed. For most operators, the mission and corresponding need has not changed.

The manufacturers themselves are positioning for resilience. The industry absorbed tariff volatility throughout 2024 and 2025 without catastrophic disruption. Supply chains that were stress-tested during the pandemic have adapted. Production planning assumes cyclical uncertainty as a baseline condition, not an aberration.

What has changed is the timeline for certain decisions. Buyers who were waiting for interest rates to drop further before committing now face a different calculation. Rates may not fall as expected. As of April 2026, rates are starting to rise. For the buyer, the aircraft they need will still be needed, and the delivery slots they opt to forfeit on a wait and see, will go to someone else.

The aviation industry has weathered oil shocks before, about one every decade actually (in 1973, in 1979, in 1990 and in 2008 to name a few). Each time, predictions of permanent decline proved premature. Each time, the market found its footing and resumed growth. The question for buyers today is not whether this cycle will end, but whether they want to be positioned when it does.

President Trump’s interest rate strategy may be in shambles. The Fed may be trapped between competing mandates. Gas prices may remain elevated through the summer and into the fall. But aircraft continue to roll off assembly lines in Wichita and Savannah and São José.

The sky that seemed so clear six months ago now carries different weather. But for those who understand that aviation markets move in cycles, and that financing decisions made during uncertainty often prove most advantageous in retrospect, the current moment offers something that periods of irrational exuberance never do: clarity about who is serious and who is merely speculating.

The Financing Landscape: What Aircraft Buyers Need to Know

The aircraft financing market has not seen such strength and credit quality in the buyer profile in years. For those well suited buyers navigating today’s uncertain rate environment, understanding the mechanics of aircraft financing has never been more important. The gap between those who secure favorable terms and those who overpay has widened as lenders recalibrate risk.

The piston aircraft market presents distinct financing dynamics. With the Cessna 172 Skyhawk remaining the industry’s most delivered single engine aircraft (191 shipped by Textron Aviation in 2025), the used market provides substantial inventory for buyers seeking training aircraft or personal transportation. This level of liquidity in the used market is part of what supports 15 to 20 year financing terms for Part 91 use, even for pre-2000 aircraft.

Flight schools evaluating fleet expansion face a particularly complex calculation. Fuel costs directly affect per-hour operating economics, student throughput, and ultimately revenue. Yet training demand tends to remain stable regardless of energy prices. People who need pilot certificates need them on schedule, not when oil markets cooperate. Schools with access to capital during uncertain periods can often acquire aircraft at more favorable prices than during boom times, when competition for delivery slots and used inventory intensifies. As noted in the FLYING Finance 2026 Flight School Fleet Optimization Guide, creating an optimal mix of aircraft can keep the new student needing to learn level flight, from burning up gas and taking a beating on that Cirrus SR20 TRAC.

The turbine segment—encompassing turboprops like the Pilatus PC-12, the Daher TBM series, and the Epic E1000, as well as the full spectrum of business jets—involves larger capital commitments and correspondingly more sophisticated financing structures. With Pilatus delivering 82 PC-12s and 50 PC-24 jets in 2025, and Daher moving 76 aircraft including its flagship TBM 960, the turboprop market has demonstrated consistent demand that financiers recognize.

Lenders evaluating turbine aircraft today are weighing several factors that have shifted since the Iran conflict began. Residual value projections (estimates of what an aircraft will be worth at the end of a financing term) now incorporate energy price uncertainty that didn’t exist six months ago. Aircraft with superior fuel efficiency may command residual premiums that make financing terms more attractive on an effective basis. Lenders that may have shied away from light sport trainers are taking a more interested view. This is good news for both the domestic disruptors like Van’s Aircraft, as well as the import disruptors like Bristell, Tecnam and Sling Aircraft.

For jets, the calculus becomes more nuanced still. Bombardier’s $7.9 billion in 2025 billings across its Challenger and Global lines, Gulfstream’s $10 billion-plus from 158 deliveries, and Embraer’s $2.5 billion from 155 aircraft shipments all reflect a market that was absorbing new production at healthy rates. Whether that absorption continues at the same pace depends partly on how corporate flight departments and charter operators respond to higher operating costs.

The Federal Reserve’s current interest rate pause creates a specific window for financing decisions. Buyers who locked in rates during the 175 basis points of cuts over the past eighteen months hold favorable positions. Those who waited for rates to fall further now face uncertainty about direction. And those considering purchases today should seek preapprovals to secure rates now while they search for their aircraft, because rates are going up.

What the data suggests is that waiting rarely proves advantageous in aviation financing. Aircraft that meet operational requirements today will meet them tomorrow regardless of what rates do. The purchase price may fluctuate modestly with market conditions. But the carrying cost of delay, in operational inefficiency, in lost productivity or in foregone opportunity, compounds while buyers hesitate.

The Q2 2026 Acquisition Checklist

- Fixed Rate Alpha: In an environment where the Fed is trapped between an oil shock and a spiky jobs report, variable rate exposure is a liability. Prioritize fixed rate capital to decouple your asset’s performance from the FOMC’s uncertainty.

- Energy Resilient Underwriting: The “Strait of Hormuz” risk premium is now permanent. If the operational ROI holds at these “War-Time” prices, you have found an airframe that outpaces the market.

- The Boardroom Proof (TCO): A pilot buys on specs; a CEO buys on Total Cost of Ownership (TCO). Use our Aircraft Ownership Calculator to move beyond the sticker price and model your cash flow. By integrating debt service, a current fuel floor, and the 100% bonus depreciation under the One Big Beautiful Bill Act, you can visualize the “True Net Cost” of your acquisition. Don’t guess your ROI. Let us help you calculate it.

- The OBBBA Tax Shield: The permanent 100% bonus depreciation under the One Big Beautiful Bill Act is your greatest hedge against inflation. A properly structured acquisition creates an immediate, first-year tax write-off that can offset the increased cost of capital.

- Slot Vetting & Churn: Actively monitor delivery “churn” in the TBM and Cirrus backlogs. As less-capitalized buyers hesitate during the Tax Day lull, high-fidelity delivery slots are opening for the first time in 24 months. Be ready to move while the market is standing still.

- The Technical PPI Firewall: In 2026, the greatest threat to your ROI isn’t just the cost of capital, it’s “Maintenance Debt.” With global supply chains still constricted by geopolitical tension, lead times for critical components are measured in months, not days. A rigorous, third-party Pre-Purchase Inspection (PPI) is your mandatory firewall. At FLYING Finance, we underwrite the integrity of the asset to ensure your capital is deployed into a flight ready tool, not a grounded project.

The manufacturers’ continued production commitments offer one form of reassurance. They are building aircraft because they expect to sell them. The financing community’s continued engagement offers another. Capital remains available for creditworthy buyers acquiring aircraft that make operational sense. What has changed is the margin for error and the premium placed on preparation.

For Flying Finance clients evaluating aircraft purchases in the current environment, the guidance remains consistent with what prudent buyers have always known: understand your operational requirements, secure appropriate financing before you need it, and make decisions based on your timeline rather than attempting to time markets that no one can predict with certainty.

The storm that disrupted President Trump’s interest rate strategy will eventually pass. The question is not whether the economy will stabilize, but whether you will have positioned yourself to benefit when it does.